The Pension Service

The Pension Service

TPS 3(16) Service

TPS 3(16) Service

- TPS Group

- Articles

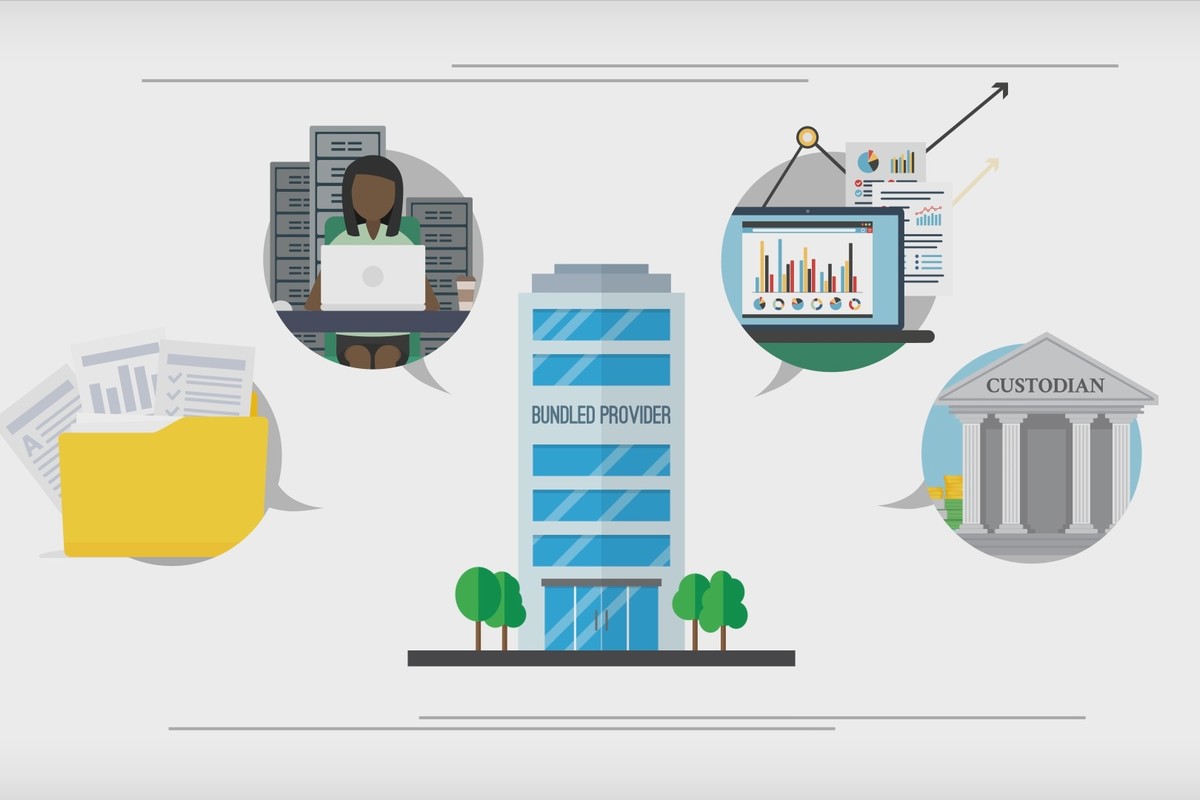

Why You Should Consider an Unbundled Retirement Plan Solution

Posted on May 6, 2026

Learn the benefits of an unbundled retirement plan over a bundled plan. Unbundled plans offer tailored services, open architecture for investment options, and personalized customer service, whereas bundled plans are standardized with limited investment options. Employers looking for flexibility, choice, quality, and customer service should consider an unbundled retirement plan.

Continue reading

The 401(k) Match True-Up to Help Employees Get the Full Match

Posted on Feb 15, 2026

Matching contributions are one of the most valuable benefits in a 401(k) plan — and employees often plan their savings strategy around getting the full match. But there’s an overlooked detail in many plans that can unintentionally reduce the match for certain participants: how the match is calculated during the year.

Continue reading

New 401(k) Contribution Limits for 2026: An Opportunity to Save More

Posted on Jan 1, 2026

The IRS has announced new contribution limits for 401(k) plans in 2026, giving retirement savers another opportunity to put more away on a tax-advantaged basis.

Continue reading

Rescuing a Forgotten 401(k): How to Track Down and Reclaim Your Old Retirement Accounts

Posted on Nov 5, 2025

It’s surprisingly easy to lose track of a 401(k) when you change jobs. In fact, millions of Americans have “orphan” accounts, which are small retirement balances left behind at former employers.

Continue reading

Why Every Employee Should Check Their 401(k) at Least Once a Year

Posted on Oct 8, 2025

It’s easy to set up a 401(k) and then forget about it, especially when life gets busy. But the “set it and forget it” approach can cost you over the long term. Checking your 401(k) at least once a year ensures your retirement savings stay on track and aligned with your goals.

Continue reading

The Four L’s of Retirement: A Framework for Peace of Mind

Posted on Sep 9, 2025

Effective retirement planning requires a holistic approach. The “Four L’s” framework—Longevity, Lifestyle, Legacy, and Liquidity—offers a structured way for employers and employees to evaluate retirement readiness and design sustainable strategies.

Continue reading

Debunking 401(k) Myths: What Small Business Owners Need to Know

Posted on Aug 18, 2025

Many small business owners hesitate to offer employees a 401(k) plan, believing it’s something only large companies can afford or manage. Unfortunately, these misconceptions can cause them to miss out on powerful benefits for both themselves and their staff.

Continue reading

Mid-Year Plan Reviews: Why Summer is the Smart Time to Assess Your 401(k) Strategy

Posted on Jul 11, 2025

Summer isn’t just for vacations—it’s also a smart time for employers to team up with their TPA for a mid-year 401(k) plan review. Taking a closer look now allows plan sponsors to catch small issues early, avoid expensive compliance problems later, and prepare for a smoother year-end.

Continue reading

For Employees: Who’s Behind Your 401(k)?

Posted on Jun 10, 2025

When it comes to your 401(k) plan, you likely know the basics: you contribute a portion of your paycheck, your employer might match some of it, and over time, your money grows for retirement. But behind the scenes, several key players are working to ensure your plan runs smoothly, and one of the most important is the Third-Party Administrator, or TPA.

Continue reading

Plan Design Strategies to Attract and Retain Talent in a Competitive Job Market

Posted on May 8, 2025

In today’s labor market, offering a competitive salary isn’t always enough to attract and retain top talent. Employees are looking for more, particularly regarding long-term financial security. One powerful but often underutilized tool is a well-designed 401(k) plan.

Continue reading